Published: February 15, 2026 | Updated: August 2, 2026

COST & COMMERCIAL VIABILITY

Run Japan’s offshore wind “promotion zones” through one common set of assumptions and the 12 zones spread from roughly 23.1 to 52.1 JPY/kWh in LCOE on the 3% real WACC used in Japanese government cost materials, or 25.0 to 57.1 JPY/kWh once withdrawal risk is priced in at 4% (levelized cost of energy: the cost per kWh generated) and from about 6.4% to below zero in IRR (internal rate of return: the project’s return on investment). The same rules and the same assumed off-take price produce that much dispersion because what drives cost here is not price or policy but site and structure. The conclusion up front: zones with strong wind and short grid and port distances, in Akita and Yamagata, lead on a relative basis, while Hokkaido zones with long grid connections face structural constraints. This pillar explains where that gap comes from, reading the market on two axes: IRR × LCOE.

→

Execution Reality

→

Bankability Test

Even under identical assumptions (30 JPY/kWh off-take, 30-year life), LCOE ranges 23.1 to 52.1 JPY/kWh at 3% real WACC and 25.0 to 57.1 at 4%, with IRR from 6.4% to negative. Wind resource, water depth, grid distance, and port distance set each project’s position through both CAPEX and OPEX.

Happo-Noshiro, Yuza, and Oga-Katagami-Akita sit in the “stronger economics” zone at ~25 JPY/kWh and 6.2 to 6.4% IRR (4% real WACC basis). Hiyama (34.4 / 2.6%) and Murakami-Tainai (33.4 / 2.7%) fall to the constrained side, weighed down by long grid connections and depth.

LCOE captures generation-cost efficiency but not payback speed or investment viability. Projects with competitive LCOE can still fail to secure adequate IRR. That is why we read the two axes together.

Wind resource cannot be improved after the fact; grid and port distances cannot be moved. These fix the achievable IRR range before any developer effort or design optimization begins.

Assumptions and How to Read This Analysis

The figures here are not definitive project returns; they are an indicative relative comparison under common assumptions. We do not rank projects or declare winners. Every number is produced by DeepWind’s viability simulator (LCOE/IRR model) using site parameters drawn from public information.

Assumptions common to all projects

- Operating life: 30 years

- Real WACC used to discount LCOE: shown on two bases, 3% (policy) and 4% (risk-adjusted) (real terms, constant 2026 JPY)

- Assumed off-take price: 30 JPY/kWh (identical for all projects)

- Exchange rate: USD/JPY 160

- Grid connection distance: straight-line distance multiplied by 1.45 to reflect transmission routing (see below)

- IRR is an unlevered project IRR (the return on the project itself, with no debt assumed). It does not depend on the discount rate

Two discount rates are shown because there are two questions. 3% is the rate used in Japanese government cost materials: it answers what the project costs society. 4% is the rate DeepWind applies once withdrawal risk is priced in, given that developers have in fact walked away from awarded projects. Reading only the first adopts the policy view of risk; reading only the second invites the response that the numbers are high because the discount rate is high. The gap between them is what this table is for. The chart and the discussion that follows are built on the risk-adjusted 4% basis, which is DeepWind’s own lens.

By deliberately removing differences in price and policy (same off-take price, same discount rate for every project), we isolate how site and structural conditions alone flow through to cost. Introducing actual bid prices or project-specific financing terms (gearing, interest rate, tenor) would change each project’s absolute values.

The IRR here is an unlevered project return. In real project finance, whether the deal secures funding turns on holding DSCR (debt-service coverage ratio) above a threshold. DeepWind’s guide is Strong ≥1.35x, Borderline 1.20 to 1.35x, Difficult <1.20x. Zones with low project IRR tend to leave thin DSCR headroom once debt is layered on, so their financing terms are tighter. This article’s IRR is the layer beneath that: the raw return the site itself allows, before leverage.

Project-specific input parameters

Each project carries its own wind resource (gross capacity factor), water depth, distance to shore, distance to the grid connection point, and distances to base and O&M ports. These feed both CAPEX and OPEX and set the project’s position on the LCOE and IRR axes. The table below lists the 12 zones from strongest economics (lowest LCOE on the 3% policy basis) down. Detailed parameters live on each project page; this pillar concentrates on the structural interpretation of the results.

Grid connection distance is the straight-line distance from the shore to the connecting substation, multiplied by 1.45 to allow for transmission routing. Off Tsugaru City in Aomori, a straight-line span of roughly 38 km corresponds to an onshore transmission line of about 55 km, running from the Tsugaru coast to Aomori City, as reported on 1 August 2026 (ATV Aomori Television). That ratio has been applied to every zone. Transmission lines avoid mountainous terrain and follow existing corridors, so straight-line distance always understates the length actually built. The degree of detour should in principle vary by terrain, but the connecting substation is undisclosed for many zones, so no zone-by-zone basis is available and a single factor is used.

| Zone | Round | LCOE policy basis 3% (JPY/kWh) |

LCOE risk-adjusted 4% (JPY/kWh) |

Project IRR (%) |

Article |

|---|---|---|---|---|---|

| Happo-Noshiro, Akita | Round 2 | 23.1 | 25.0 | 6.4 | View |

| Yuza, Yamagata | Round 3 | 23.3 | 25.3 | 6.2 | View |

| Oga-Katagami-Akita, Akita | Round 2 | 23.7 | 25.6 | 6.2 | View |

| Noshiro-Mitane-Oga, Akita | Round 1 | 24.6 | 26.6 | 5.5 | View |

| Choshi, Chiba | Round 1 | 25.5 | 27.7 | 5.0 | View |

| Yurihonjo, Akita | Round 1 | 26.0 | 28.2 | 4.7 | View |

| Tsugaru, Aomori | Round 3 | 26.7 | 29.1 | 4.3 | View |

| Saikai-Enoshima, Nagasaki | Round 2 | 26.9 | 29.3 | 4.3 | View |

| Matsumae, Hokkaido | Round 4 (expected) | 29.9 | 32.8 | 3.0 | View |

| Murakami-Tainai, Niigata | Round 2 | 30.7 | 33.4 | 2.7 | View |

| Hiyama, Hokkaido | Round 4 (expected) | 31.3 | 34.4 | 2.6 | View |

| Goto, Nagasaki (Floating) | Promotion zone | 52.1 | 57.1 | -2.7 | View |

Reading the Promotion Zones on IRR × LCOE

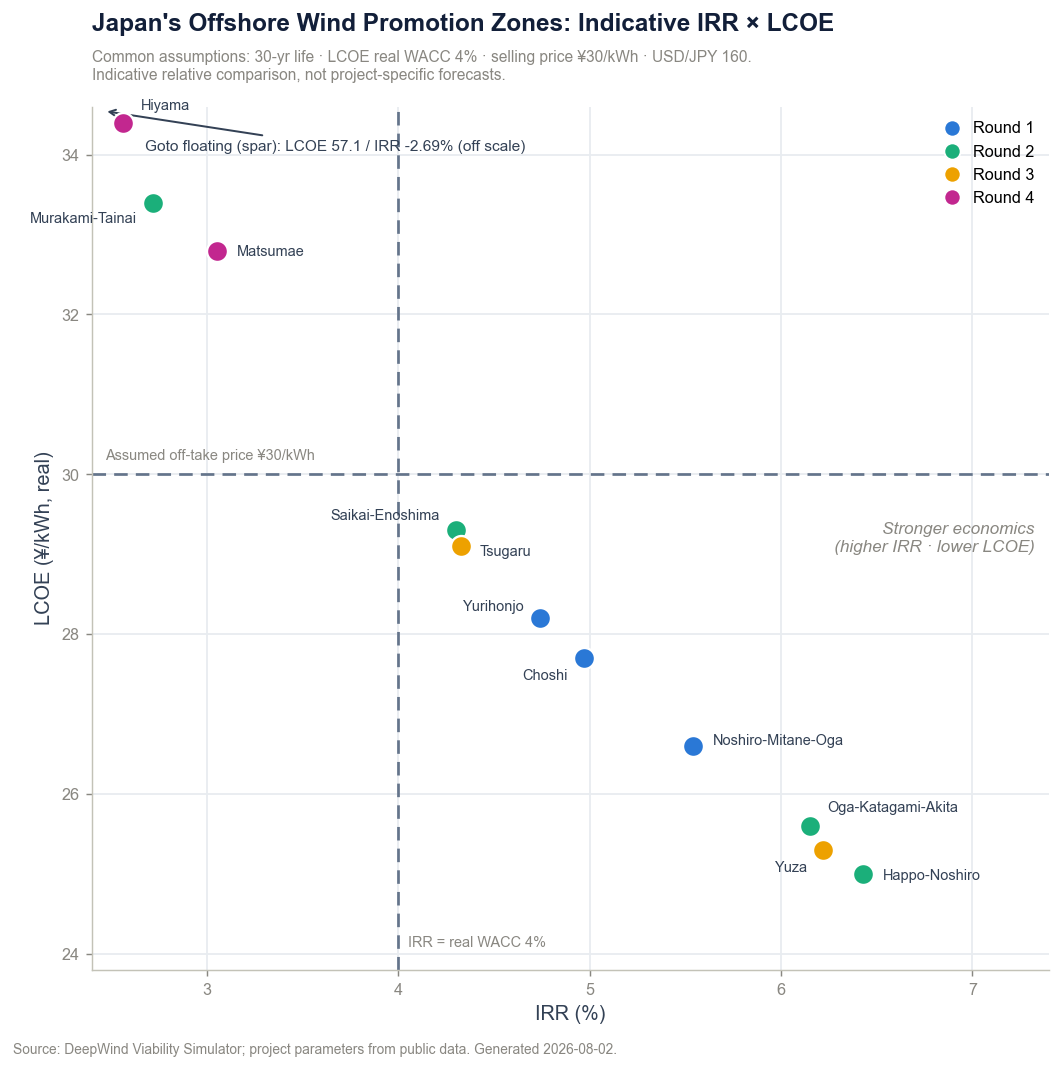

Figure 1: Relative economics of the promotion zones (IRR × LCOE)

IRR on the horizontal axis, LCOE on the vertical; lower-right (high IRR, low LCOE) is relatively stronger. The dashed lines mark the ¥30 assumed off-take price and the 4% real WACC. Only zones to the lower-right of the crosshair earn above their cost of capital under these assumptions. Colour marks the round. Goto (floating; 57.1 / −2.7%) sits beyond the chart range and is noted by the arrow. This chart uses the risk-adjusted 4% real WACC basis.

Source: DeepWind Viability Simulator, 2026-08. Assumptions: 30-yr life, 4% real WACC (risk-adjusted case), 30 JPY/kWh, USD/JPY 160, grid distance = straight line × 1.45.

Why evaluate LCOE and IRR together?

LCOE is an effective measure of generation-cost efficiency, but it does not directly reflect how quickly the initial investment is recovered, the timing mismatch between spending and revenue, or the ultimate viability of the project as an investment. IRR captures those. In Japan’s market, projects with competitive LCOE have still struggled to secure adequate IRR, so we focus on the relationship between the two. On the scatter, projects toward the lower-right are “low cost and high return” and relatively strong; those toward the upper-left are more constrained.

The dashed crosshair carries a precise meaning. Under these assumptions (¥30 off-take, 4% real WACC), LCOE below ¥30 and IRR above 4% are the same boundary. It is the line where the assumed price exactly covers the cost of capital. Eight of the twelve zones sit inside it (lower-right): the fixed-bottom clusters in Akita, Yamagata, and Chiba, followed by Tsugaru in Aomori and Saikai-Enoshima in Nagasaki. The four that remain outside are grid-distant Matsumae, Hokkaido (32.8 / 3.0%), depth-and-distance-constrained Murakami-Tainai (33.4 / 2.7%), Hiyama, Hokkaido (34.4 / 2.6%), a zone spanning two sea areas with a long grid run, and floating Goto. Matsumae and Tsugaru fall on opposite sides of the line by a small margin, a reminder that strong wind can still lose to grid distance or water depth.

What the strong Akita and Yamagata zones share

The lower-right zone (high IRR, low LCOE) holds Happo-Noshiro, Akita (25.0 / 6.4%), Yuza, Yamagata (25.3 / 6.2%), and Oga-Katagami-Akita (25.6 / 6.2%), on the 4% risk-adjusted basis. Three things are common to them:

- Robust wind resource (high capacity factor). A stable energy yield underpins revenue even at a fixed off-take price. Wind resource cannot be improved after the fact; it pre-sets the ceiling on achievable IRR.

- Relatively shallow water and workable installation conditions. Fixed-bottom foundations (anchored to the seabed) can be designed efficiently, containing foundation and installation cost.

- Proximity to grid and O&M ports. Yuza sits about 7 km from its grid connection and Happo-Noshiro about 8 km, cutting both the upfront transmission cost and long-run O&M cost.

The constrained Hokkaido and Niigata zones

The upper-left (high LCOE, low IRR) holds Hiyama, Hokkaido (34.4 / 2.6%), Murakami-Tainai, Niigata (33.4 / 2.7%), and Matsumae, Hokkaido (32.8 / 3.0%). All three carry an LCOE well above the Honshu shallow-water zones and, under these assumptions, do not cover the ¥30 assumed off-take price.

The single biggest reason these zones carry higher LCOE than the Honshu shallow-water zones is distance to the grid connection point. Matsumae is about 116 km out once routing is allowed for, and the onshore transmission line stretches accordingly, raising CAPEX structurally. Hiyama is the only promotion zone spanning two separate sea areas, with grid distances of about 73 km and 132 km (this analysis averages the two, treating it as ~102 km grid distance and ~47 m depth). Wind resource is actually strong at both (capacity factor ~49.8% at Hiyama, ~48.2% at Matsumae), but transmission and installation cost eat that advantage, lifting LCOE into the low ¥30s. Across all three, a single factor, grid distance, pre-sets the ceiling on economics before any design optimization.

These are not problems that developer effort or design optimization alone can solve. The site conditions themselves fix the achievable IRR range in advance.

Conditions get harder as the rounds progress

Grouped by auction round, the data also shows how the development phase is shifting. Rounds 1 and 2 cluster in favorable areas, with LCOE roughly 24 to 26 JPY/kWh and IRR around 6 to 7% (Happo-Noshiro, Oga-Katagami, Noshiro-Mitane-Oga). In Round 3, some projects keep strong economics (Yuza) while others slip to mid-pack as distance bites (Tsugaru, 27.3 / 5.1%). The expected Round 4 Hokkaido zones (Matsumae, Hiyama) mark a move into geographically harder waters. The market is shifting from the “low-hanging fruit” toward more constrained sites.

Why Goto (floating) is an outlier

Goto City sits far off the other 11 zones at 57.1 JPY/kWh and −2.7% IRR on the 4% basis (52.1 JPY/kWh at the 3% policy basis). The reason is not bid price but technology. Goto is the only floating project (spar-type); its structural cost, including the float and mooring, is materially higher than fixed-bottom, and at the same 30 JPY/kWh off-take it does not pencil out. Floating wind is essential to opening Japan’s deep-water sites, but its cost level sits on a different plane from fixed-bottom. Goto is therefore not a project to rank side-by-side with the 11 fixed-bottom zones; it belongs to the separate topic of floating cost reduction, which we cover in depth in the related article.

👉 Floating Offshore Wind Cost Structure and LCOE Reality

Promotion-zone economics are set first by site, not by price or policy.

Line every project up at the same off-take price and the same discount rate, and LCOE still spans the mid-20s to 54 JPY/kWh and IRR from 7% to negative. What that says is that the main driver of Japanese offshore wind viability sits upstream of price negotiation or financing skill: the unmovable site conditions of wind, water depth, grid distance, and port distance. Distance to the grid connection point, in particular, is strong enough to cancel out a good wind resource.

This structure carries implications on both the policy and execution sides. For policy, it means transmission build-out and the design of grid-connection cost allocation directly shape the viability gap between zones. For developers, it means evaluating a site on wind resource alone risks missing the grid and port cost penalties that follow. As the promotion-zone program expands, the decisive question is not wind potential alone but how realistically the full cost structure, grid and port included, can be designed to bring the constrained zones’ LCOE down while sustaining IRR. The Akita and Yamagata shallow-water zones already reach the mid-20s JPY/kWh; the remaining challenge is how far the deeper, grid-distant zones can follow. These figures are a relative comparison under standardized assumptions; a sensitivity analysis incorporating execution delay, material prices, and financing terms is handled separately. The structural point, that site sets the skeleton of viability, holds even as the assumptions move.

Frequently Asked Questions

Related DeepWind Articles

- Floating Offshore Wind Cost Structure and LCOE Reality

- Yuza Offshore Wind: Zero-Premium Bidding and Bankability

- Floating Offshore Wind in Japan: Market Structure, Costs, and Policy

- Japan’s Offshore Wind Technology Roadmap 2026

DeepWind Weekly tracks Japan’s offshore wind market beyond headline announcements, focusing on execution risk, cost structure, project viability, supply-chain constraints, and policy implications.

Subscribe to receive weekly intelligence on Japan’s offshore wind market.

Why Isn't Floating Wind Bankable in Japan Yet?

The synchronized supply-chain bottleneck, quantified node by node, with a full sensitivity ranking and a bankability ladder of scaling conditions. Includes Simulator Professional (β) access to reproduce every figure on your own assumptions.

See the full analysis →