Published: January 11, 2026 | Updated: June 17, 2026

POLICY & REGULATION

Japan has built one of Asia’s most legible offshore wind policy frameworks — long-term capacity targets, a dedicated sea area utilization law, competitive auctions, and structured revenue support through FIT and FIP. The participation conditions are clearly defined. Yet the market has also produced project withdrawals, repeated schedule revisions, and a Round 1 record that raised fundamental questions about the gap between awarded capacity and deliverable capacity. Understanding Japan’s offshore wind framework means understanding both what it provides — procedural certainty — and what it was never designed to provide: execution certainty.

This article maps the framework across eight structural layers, from national targets through the March 2026 guideline revisions. The goal is a working reference for reading policy signals, not a regulatory checklist. For 2026-specific auction reform details, see the dedicated article: Japan Revises Its Offshore Wind Auction Guidelines (June 2026).

→

Execution Reality

→

Bankability Test

Japan’s framework excels at defining participation rules — zone designation, auction selection, revenue support eligibility. What it does not provide, and was not designed to provide, is assurance that awarded projects will be delivered on schedule and within bid assumptions. That distinction is the most important analytical frame for reading any Japan offshore wind policy signal.

National targets, the Marine Renewable Energy Act, auction design, FIT/FIP, LTDA, EEZ expansion, certification standards, and base port rules all follow the same structural logic: government defines access conditions; market participants bear execution risk. No layer in the framework transfers supply chain, construction cost, or grid connection risk to the government.

The March 2026 Promotion Zone Guideline revisions — viability screening indicators, centralized environmental impact assessment, shipping lane formalization — materially reduce early-stage developer burden. They do not change the post-award risk distribution. Construction cost volatility, vessel availability, and grid connection economics remain developer-side variables with no framework backstop.

Extending the legal framework into Japan’s Exclusive Economic Zone expands the theoretical resource envelope, particularly for floating wind. But EEZ deployment timelines depend on technology maturity, floating platform supply chain development, and grid economics that cannot be resolved by legal reform alone. For the 2030 target window, EEZ capacity is not a material contribution.

1. Overall Structure: Policy Signals and Their Limits

Japan’s offshore wind policy follows a clear structural logic focused on enabling market entry through institutional design. From an early stage, the government adopted a step-by-step approach: setting quantitative capacity targets, establishing a legal framework for sea area use, and introducing competitive auction mechanisms to allocate development rights. Each step reduces one category of uncertainty while leaving others to market resolution.

As a result, Japan’s offshore wind market has transitioned from one characterized by high policy uncertainty to one where the participation framework is relatively well defined. This shift has played a critical role in attracting domestic and international developers, suppliers, and financial institutions. The risk profile has shifted — but not disappeared.

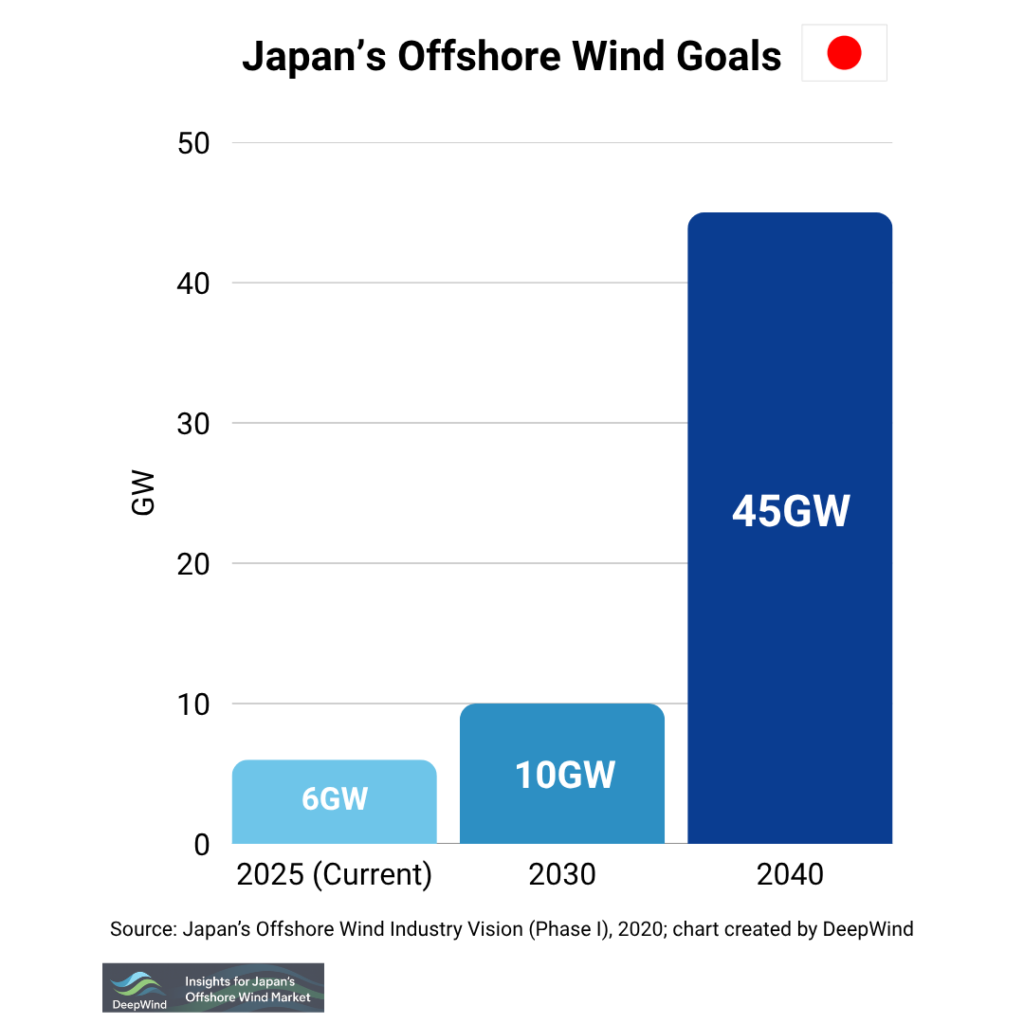

1.1 The 2030 and 2040 Capacity Targets as Market Signals

Japan’s offshore wind capacity targets function as policy commitment signals rather than operational plans. Source: METI Strategic Energy Plan, DeepWind analysis.

Japan’s offshore wind capacity targets for 2030 and 2040 are not merely power-mix contributions; they communicate a long-term government commitment to positioning offshore wind as a core power source. For market participants, these targets have functioned as investment signals justifying early-stage market entry, supply chain localization planning, and long-term strategic positioning by developers and manufacturers.

The signal value of targets depends on whether downstream execution conditions can support delivery. When the gap between target and deliverable capacity is large — as Round 1 outcomes suggested — the credibility signal weakens. Policy-following requires reading targets alongside execution track records.

👉 Japan’s Offshore Wind Goals for 2030 & 2040: What the Numbers Mean for Market Participants

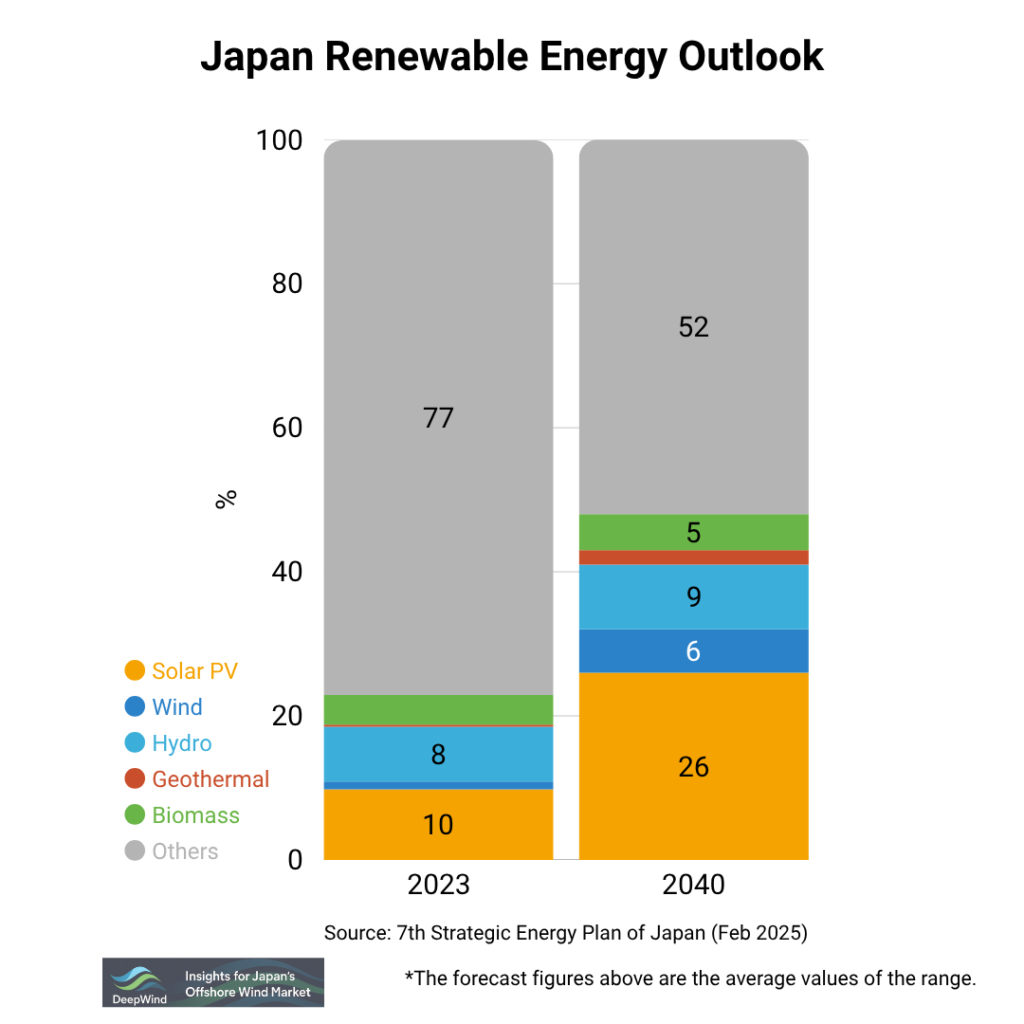

1.2 Offshore Wind in Japan’s Strategic Energy Plan

Offshore wind’s share in Japan’s 2040 power mix target, from the 7th Strategic Energy Plan. Source: METI, DeepWind analysis.

Within Japan’s Strategic Energy Plan (第7次エネルギー基本計画), offshore wind is positioned as a future core power source, with strategic importance spanning decarbonization, energy security, and industrial competitiveness. The Energy Plan functions as a directional framework — it establishes priorities and long-term intent but does not resolve execution-stage challenges such as cost escalation, supply chain constraints, or project-specific risk allocation.

For offshore wind market participants, the Strategic Energy Plan’s primary value is confirming that Japan’s commitment to the sector is embedded in national energy strategy rather than contingent on any single ministry’s discretion. Execution risk, however, sits below the strategic level.

👉 Japan’s Energy Plan (Strategic Energy Plan) Explained

2. The Marine Renewable Energy Act: Sea Area Use Rights and Their Practical Limits

The cornerstone of Japan’s offshore wind framework is the Marine Renewable Energy Act (再エネ海域利用法), which provides the statutory basis for long-term and effectively exclusive use of designated sea areas for offshore wind projects. By clarifying sea area use rights and formalizing selection procedures, the Act established the legal conditions needed for long-horizon private investment — a prerequisite for project financing at offshore wind scale.

The Marine Renewable Energy Act is designed to provide access and procedural certainty: government-led area preparation, competitive selection, and long-term occupation rights consistent with international offshore wind practice. It does not, by design, resolve execution-stage conditions — supply chain capacity, construction constraints, financing terms, or cost volatility. Those factors are shaped by downstream mechanisms and market conditions, not by the Act itself.

2.1 Design Logic: What the Act Provides and What It Stops Short Of

The design logic is straightforward: government-led area preparation reduces uncertainty around site availability and procedures; competitive selection allocates development rights on a transparent basis; and long-term occupation arrangements support the investment time horizon typical for offshore wind projects (typically 20–30 years). This framework lowers the participation threshold for market entry significantly compared to a system without defined sea area use rights.

Critically, the Act’s role is to establish access and procedural certainty, not execution certainty. A developer holding a Promotion Area designation has cleared the access hurdle — but still faces the full suite of execution variables that determine whether a project reaches financial close, construction, and commissioning.

👉 Japan’s Offshore Wind Legal Framework: The Marine Renewable Energy Act

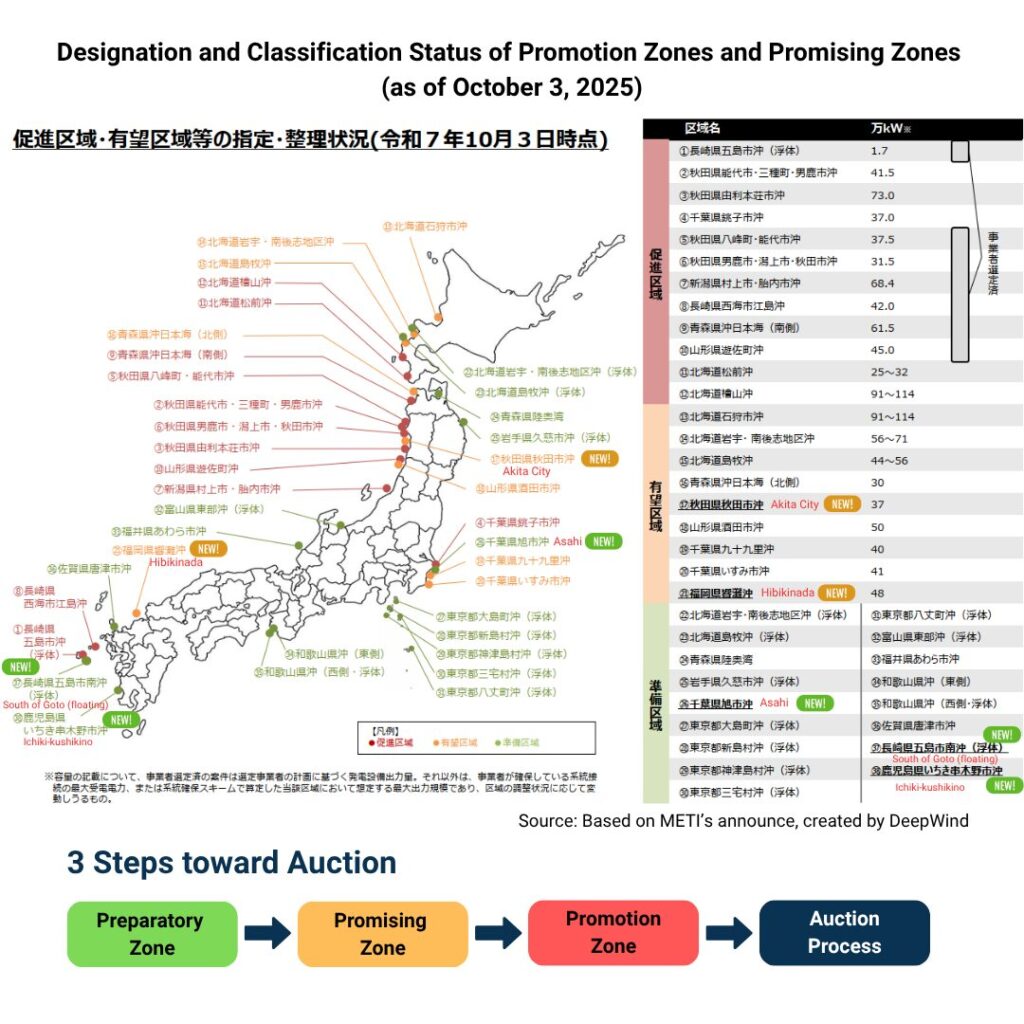

2.2 Area Designation: What “Being Designated” Actually Means for Market Participants

Zone designation status as of October 2025, showing the progression from promising area through promotion zone auction eligibility. Source: METI, October 2025.

Under the Marine Renewable Energy Act, sea areas progress through stages of preparation — preparation zones, promising areas, and finally promotion areas — before becoming auction-eligible. Each stage involves government review, stakeholder coordination, and procedural confirmation. The process is designed to reduce early-stage uncertainty and ensure that auctioned zones have been assessed for basic viability conditions.

From a market perspective, promotion area designation marks the start of competition, not an assurance of project viability. Once an area becomes auction-eligible, key differentiators shift toward bid competitiveness, deliverability assumptions, and execution readiness — factors not determined by designation alone. A designated area with poor wind resources, difficult grid access, or conflicting maritime uses will not become commercially viable through designation alone.

👉 Japan’s Offshore Wind Promotion Zones: A Complete Project List and Structural Market Analysis

👉 Japan’s Offshore Wind “Preparation Zone” Projects

3. Auction Design: How Japan Allocates Development Rights

With the Marine Renewable Energy Act establishing the legal backbone for sea area use, Japan’s offshore wind sector entered a stage where projects could be formed through a defined process. The auction framework determines how development rights are allocated — and how competition is structured shapes developer behavior, risk-taking, and the stability of post-award execution plans.

3.1 The Centralized Method: Government-Led Preparation Before Competition

The centralized method (集中管理方式) represents a major evolution in Japan’s auction design. By conducting key surveys and preparatory work on the government side — wind resource assessment, environmental surveys, grid connection studies — and then running auctions based on a standardized information set, the method aims to reduce early-stage uncertainty and lower barriers to entry by equalizing information access across bidders.

The centralized method changes where execution risk surfaces in the project lifecycle, not whether that risk exists. By standardizing pre-auction surveys, it reduces early-stage uncertainty and lowers developer entry costs. But post-award risks — procurement cost escalation, installation vessel availability, grid connection delays, and construction sequencing constraints — remain developer-side variables that the centralized framework does not absorb. Most material uncertainties in Japan’s offshore wind projects have emerged after project selection.

👉 Centralized Method in Japan Offshore Wind: What It Means for Project Development

3.2 Scoring and Evaluation Criteria: Beyond Simple Price Competition

Japan’s auctions are structured to evaluate proposals using multiple criteria — not only price but also project plans, local engagement, supply chain localization commitments, and implementation capability. The intent is to avoid purely price-driven outcomes and to incorporate broader deliverability and value considerations into developer selection.

Scoring-based evaluation systems are, by design, tools for comparing plans at a specific point in time. They assess consistency, preparedness, and proposed execution frameworks under a defined set of assumptions. However, offshore wind projects unfold over long timelines and are exposed to external factors that cannot be fully captured at the bidding stage. Changes in costs, supply availability, or construction conditions can widen the gap between bid-time evaluations and build-time realities, even for projects that performed well under the scoring framework.

Japan’s post-Round 1 experience showed that high bid scores did not translate directly into delivery performance. This observation drove the subsequent reforms to evaluation criteria and auction design described in Section 6.

👉 Japan Offshore Wind Scoring System: Project Selection Criteria Explained

4. Revenue Framework: FIT, FIP, and Long-Term Decarbonization Auctions

Alongside auction design, revenue stability is one of the most important determinants of offshore wind project bankability. The core question for lenders and equity investors is how electricity can be sold — at what level of certainty, for what duration, and under which market exposure profile. These parameters influence not only project economics but also lender risk assessment, DSCR calculations, and investment decision-making.

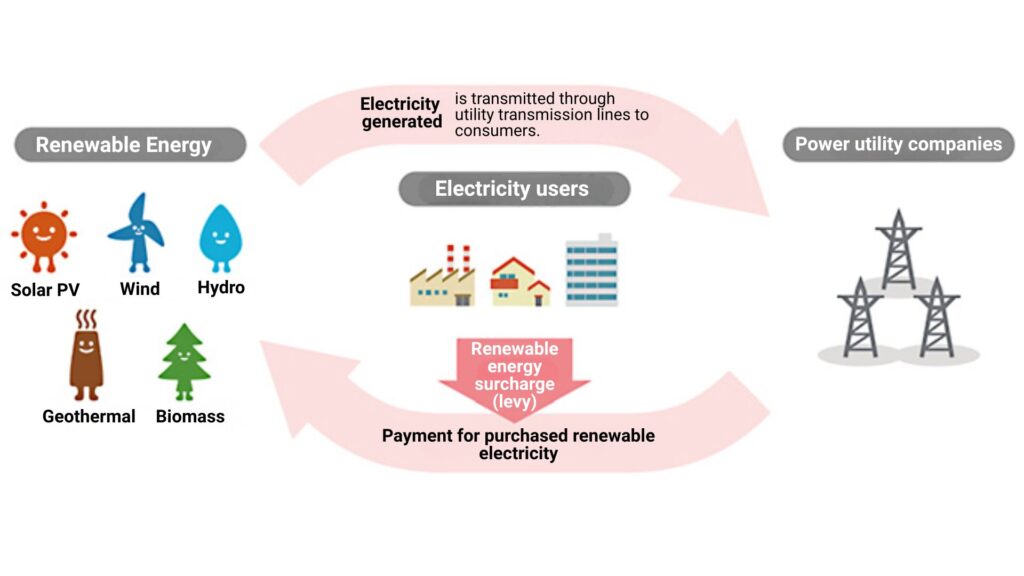

4.1 FIT to FIP: What the Transition Changes at the Framework Level

FIT provides a fixed purchase price; FIP provides a premium on top of market price. The transition shifts market exposure to developers while maintaining government revenue support. Source: METI, DeepWind analysis.

Japan initially used FIT (Feed-in Tariff: a fixed-price purchase guarantee) to reduce revenue uncertainty and accelerate renewable deployment. As deployment expanded, policy focus shifted toward market integration and cost discipline. This led to the introduction of FIP (Feed-in Premium: a variable premium added on top of market sales revenue), which maintains government support while exposing developers to market price signals.

From a project finance perspective, the FIT-to-FIP transition increases revenue exposure to market price volatility. Under FIP, the total realized revenue depends on both the premium level and market price movements, which introduces a basis risk element that was absent under FIT’s fixed tariff structure.

👉 FIT vs FIP in Japan: How Renewable Revenue Support Works

4.2 Long-Term Decarbonization Auctions: A Complementary Revenue Mechanism

Japan’s long-term decarbonization auction (LTDA, 長期脱炭素電源オークション) is designed to support long-horizon investment in low-carbon power by providing additional capacity revenue under defined conditions, separate from the energy revenue stream. For offshore wind projects, LTDA participation can improve long-term cash flow visibility by adding a capacity payment layer to the FIP revenue base.

FIP combined with LTDA capacity payments improves project revenue stability compared to FIP alone — but this addresses only one dimension of lender risk. DSCR ≥1.35x for offshore wind projects also depends on P90 energy yield confidence, construction cost certainty (contingency assumptions), debt service coverage through the construction period, and refinancing risk at the FIP contract end. Japan’s revenue framework improves the revenue-side inputs to project finance models; it does not reduce cost-side uncertainty. Projects relying on aggressive capacity factor assumptions or optimistic construction cost inputs remain exposed to DSCR <1.20x scenarios.

👉 Japan’s Long-Term Decarbonization Auction (LTDA): A Complete Guide

👉 Corporate PPA in Japan: Structures, Pricing, FIP Policy & Offshore Wind Connection

5. Expanding the Framework: EEZ, Certification, Port Rules, and Zone Selection Reform

Policy and regulatory work in Japan’s offshore wind sector is not limited to operating existing mechanisms. Several parallel tracks are being refined or extended as the market moves deeper into the execution phase: EEZ expansion, certification standards, base port utilization rules, and zone selection procedures. Each shapes conditions under which projects can be planned, financed, and delivered — often in ways not fully captured by the core legal and auction framework alone.

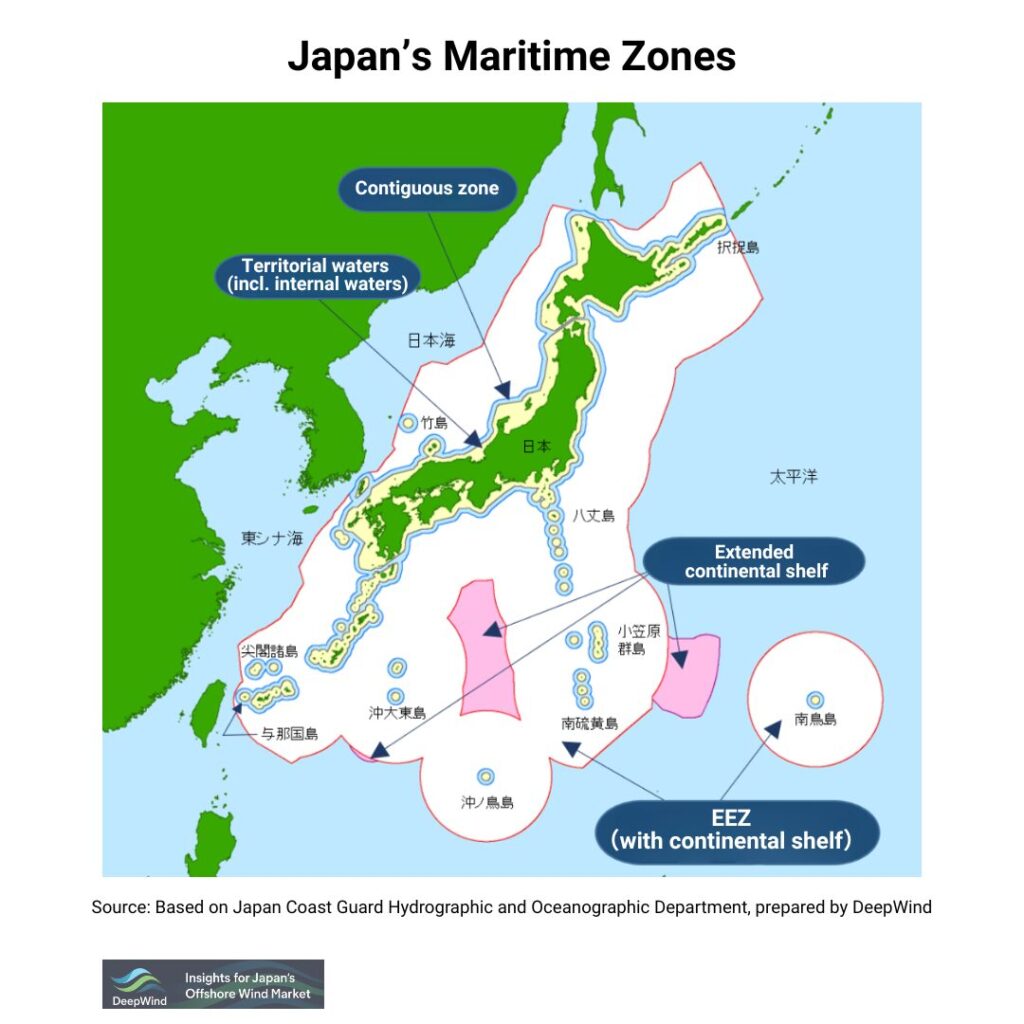

5.1 EEZ Expansion: Long-Term Resource Option, Not Near-Term Pipeline

Japan’s EEZ encompasses deep-water areas requiring floating wind technology. Legal access reform is the necessary first step, but not sufficient for near-term deployment. Source: DeepWind analysis.

Expanding offshore wind development into Japan’s Exclusive Economic Zone (EEZ) could widen long-term development options and increase theoretical available capacity, particularly for floating wind. EEZ projects typically involve deeper waters (>200m in many areas), greater reliance on floating platform technology, and longer logistics and grid connection distances than nearshore territorial sea development.

For this reason, EEZ expansion is best understood as a long-term capacity option rather than a near-term contribution to the 2030 target pipeline. Legal reform enabling EEZ development (enacted April 2026) is a necessary condition for floating wind at scale in Japan. It is not sufficient: practical deployment timelines will depend on technology maturity (particularly floating platform supply chain localization), port infrastructure for deep-water installation, and grid connection economics for far-offshore sites.

👉 Japan Offshore Wind EEZ Law Revision: What’s Being Discussed

👉 Japan’s Offshore Wind Technology Roadmap 2026: From Coastal Foundations to EEZ Commercialization

5.2 Standards, Certification, and Regulatory Practice

Offshore wind is a highly internationalized industry, with many technologies and design practices aligned with global standards (IEC, DNV, ClassNK). In Japan, project development also involves domestic legal requirements, safety rules (particularly under the Electrical Business Act and related regulations), and certification processes under ClassNK and METI guidelines. These factors influence timelines and execution planning, depending on how they apply to project-specific designs and procurement strategies.

For international developers and component suppliers, understanding the intersection between global type certification and Japan’s domestic approval framework is a material execution planning question. Projects that assume direct transferability of internationally certified equipment without Japan-specific verification steps have encountered delays.

👉 Japan Offshore Wind: Certification and Regulatory Challenges Explained

5.3 Base Port Utilization Rules: The “Software” Layer of Port Infrastructure

Public discussion of port infrastructure for offshore wind has historically focused on hardware constraints — quay length, water depth, and ground bearing capacity. For developers and lenders structuring projects, however, the rigidity of lease terms, restoration obligations, and multi-port coordination rules (the “software” layer) has often been a more material constraint on investment decisions than physical port specifications.

At the January 2026 Study Group on Port Infrastructure, MLIT presented five operational improvements under review: reducing the contract guarantee burden on the first developer to use a port; introducing a lease-fee suppression period before commercial operation; relaxing restoration obligations for privately funded port upgrades; equalizing lease fees among neighboring base ports; and accommodating simultaneous use of multiple ports under coordinated lease terms. These proposals target cost uncertainty in project finance structuring and aim to encourage private investment in port upgrades needed for the floating wind era.

Hardware expansion takes physical time; rule revision can be implemented on a shorter horizon. The move to address the software side of port utilization marks a meaningful shift in how execution-stage bottlenecks are being approached at the policy level.

👉 MLIT Base Port Operational Improvements: Five Changes Under Review

5.4 Promotion Zone Guideline Revision (March 2026): Three Structural Changes

In March 2026, METI, MLIT, and the Ministry of the Environment jointly published proposed revisions to the Promotion Zone Designation Guideline and the Centralized Method operational policy, as institutional preparation for the amended Marine Renewable Energy Act taking effect April 1, 2026. The revisions introduce three structural changes to the zone selection process.

First, viability screening indicators: Reference benchmarks have been introduced for wind speed (NeoWins — NEDO’s national offshore wind resource database — annual average at 140m hub height), water depth, and onshore transmission line distance. These are not hard cutoffs but provide explicit reference points for the “comprehensive assessment” previously applied at the promising-area screening stage. Zones with weaker fundamentals face higher justification thresholds in subsequent rounds.

Second, centralized environmental impact assessment: The early stages of the environmental impact assessment (scoping and methodology) shift from developer-led to government-led. The Ministry of the Environment will now conduct marine environmental surveys prior to promotion zone designation. This materially reduces pre-auction developer burden on what had been one of the highest-cost and highest-uncertainty phases of project development.

Third, shipping lane setback formalization: The classification of a candidate area as a “promising area” now explicitly requires that views from relevant shipping industry associations and operators have been sufficiently confirmed. No fixed minimum distance is prescribed; setbacks are determined case-by-case through stakeholder coordination. This gives the maritime industry a formal procedural role in zone progression that did not previously exist.

Taken together, these revisions move zone selection toward greater specificity — replacing previously ambiguous criteria with explicit benchmarks, defined responsibilities, and structured stakeholder requirements. For developers, they both lower certain early-stage burdens and introduce new gating conditions that must be reflected in pipeline strategy.

For the June 2026 auction guideline revisions (price floor introduction, feasibility reweighting, schedule flexibility), see the dedicated article below:

6. From Project Withdrawals to Policy Updates: Key Milestones in Framework Evolution

Japan’s offshore wind framework is not static — it evolves through implementation experience, market feedback, and political economy adjustments. The Round 1 withdrawal events were the most significant single catalyst for policy revision since the Marine Renewable Energy Act’s introduction. Understanding the trajectory from Round 1 through the 2026 reforms provides context for interpreting current policy signals.

6.1 Round 1 Withdrawals: What They Revealed About the Framework

In Round 1, a subset of awarded offshore wind projects later faced significant implementation challenges, resulting in withdrawal decisions in some cases. These events drew attention to the gap between bid-time planning and build-time reality — specifically, the inability of the auction framework to screen for genuine execution readiness rather than plan quality alone. METI’s withdrawal analysis identified a combination of cost escalation, supply chain constraints, and post-award schedule adjustment as contributing factors.

👉 Round 1 Withdrawals: METI Analysis and Key Takeaways

6.2 Post-Round 1 Policy Adjustments and 2026 Reforms

Following Round 1 outcomes, Japan advanced a sequence of policy discussions and updates aimed at strengthening the execution environment and improving auction design. These include adjustments to evaluation criteria weighting (reducing price score dominance), feasibility verification requirements, and the introduction of schedule flexibility provisions in the June 2026 auction guideline revisions.

Key reference articles for 2026-specific reforms:

- Japan Offshore Wind Auction Reform (2026): Structural Changes and Market Implications

- Japan Offshore Wind Policy Updates (2026): Integrated Summary

- What Has Changed in Japan’s Offshore Wind Policy? (2025 Review)

- Japan Revises Its Offshore Wind Auction Guidelines (June 2026): Price Floor, Feasibility Reweighting, and Schedule Flexibility

7. What the Framework Covers — and What Sits Beyond It

Japan’s offshore wind framework provides the essential elements for market participation: policy direction, legal procedures for sea area use, auction-based allocation mechanisms, and revenue-support structures. Together, these elements improve predictability and enable market players to plan within a defined set of rules. The framework is well-designed for what it was designed to do.

At the same time, offshore wind execution depends on factors that sit beyond any single policy or regulatory framework. Supply chain availability, construction vessel capacity, cost and financing conditions, grid development pace, and project-specific site constraints are shaped by broader market dynamics and project-level decision-making. The framework provides the starting conditions for execution; it does not guarantee execution outcomes.

No policy intervention can substitute for physical supply chain capacity. Japan’s offshore wind framework — including the 2026 revisions — addresses institutional bottlenecks: zone selection speed, environmental assessment burden, and auction evaluation design. It does not address physical bottlenecks: the number of installation vessels available for Japanese projects, the output rate of domestic turbine nacelle facilities, or the pace of subsea cable manufacturing capacity expansion. For the 2030 pipeline, the binding constraints are increasingly physical, not institutional.

For readers, the key analytical implication is that a practical reading of Japan’s offshore wind policy requires identifying what assumptions the framework relies on and what risks must be evaluated outside the formal rules. A well-structured framework and a well-structured project are related but distinct conditions.

8. Reading the Framework: What Each Layer Covers and Where Execution Risk Begins

Japan’s offshore wind policy and regulatory framework provides a structured, legible set of participation rules that compares favorably with comparable markets in Asia. National targets signal long-term commitment; the Marine Renewable Energy Act provides sea area use rights; auction mechanisms allocate development rights on competitive terms; FIT/FIP/LTDA structures provide revenue support; and the 2026 revisions are systematically narrowing remaining front-end uncertainties.

The framework’s limitations are structural, not incidental. It is designed to provide access and procedural certainty — not to guarantee that awarded projects will be built on time, within budget, or at the assumed capacity factor. Post-award risk distribution sits with developers and their lenders. That distribution is unlikely to change materially through further framework revision alone.

For market participants, the practical implication is to use the framework as a foundation for risk identification, not as a risk resolution mechanism. What the framework covers clearly establishes the participation baseline. What it does not cover identifies where genuine commercial and technical judgment is required.

Key Framework Signals to Monitor

- How Round 4 auction evaluation criteria weighting is finalized — specifically whether feasibility verification requirements are robust enough to screen for genuine execution readiness

- Whether grid development pace (particularly offshore grid corridor development) aligns with project commissioning schedules across the Promotion Area pipeline

- How effectively the centralized EIA process reduces pre-auction timeline uncertainty in practice vs. what the policy revision intended

- The pace at which EEZ legal framework expansion translates into actionable Promotion Area designations for floating wind

Japan’s offshore wind framework is increasingly well-designed. Japan’s offshore wind execution gap is not a framework problem.

The policy and regulatory architecture Japan has built for offshore wind is substantively complete. The Marine Renewable Energy Act provides legal sea area access; competitive auctions allocate development rights; FIT/FIP/LTDA structures provide revenue support; the 2026 revisions are systematically narrowing front-end uncertainty. Institutional bottlenecks are being addressed with real policy effort. This is not a market that lacks a regulatory framework.

The execution gap — the distance between awarded capacity and commissioned capacity — is not a framework failure. It is a physical and commercial constraint operating below the policy layer. Installation vessel availability for Japanese projects is structurally limited. Domestic turbine nacelle capacity is expanding but constrained by industrial planning horizons that exceed any single auction cycle. Floating wind platform supply chains do not yet exist at commercial scale in Japan. These are not problems that guideline revisions, viability screening benchmarks, or centralized EIA processes can solve directly.

The implication for market reading: when assessing Japan offshore wind policy developments, the analytically productive question is not “does the framework support this project?” — for most projects in designated Promotion Areas, it does. The productive question is “does the physical and commercial supply capacity exist to execute this project at the timeline and cost assumptions embedded in the bid?” That question is answered by supply chain analysis and project finance stress-testing, not by policy documents.

Frequently Asked Questions

Related DeepWind Articles

- Japan’s Offshore Wind Legal Framework: The Marine Renewable Energy Act

- Centralized Method in Japan Offshore Wind: What It Means for Project Development

- FIT vs FIP in Japan: How Renewable Revenue Support Works

- Japan’s Long-Term Decarbonization Auction (LTDA): A Complete Guide

- Japan Revises Its Offshore Wind Auction Guidelines (June 2026)

- Round 1 Withdrawals: METI Analysis and Key Takeaways

- Japan’s Offshore Wind Technology Roadmap 2026: From Coastal Foundations to EEZ Commercialization

DeepWind Weekly tracks Japan’s offshore wind market beyond headline announcements, focusing on execution risk, cost structure, project viability, supply-chain constraints, and policy implications.

Subscribe to receive weekly intelligence on Japan’s offshore wind market.