Published: May 18, 2025 | Updated: June 18, 2026

POLICY & REGULATION

Japan’s Strategic Energy Plan is the top-level document that sets the direction of national energy policy — and the reference point every offshore wind target traces back to. The 7th edition, approved by the Cabinet in February 2025, commits Japan to carbon neutrality by 2050, raises renewables to around 40–50% of the FY2040 power mix, and lifts wind power from 1.1% of generation today to a 4–8% range. The plan itself carries no legal enforcement, but its numbers function as a binding signal for corporate strategy, investment decisions, and local planning. This article explains how the plan is built, what the 7th edition changed, and exactly where offshore wind sits within it.

👉 Japan’s Offshore Wind Policy & Regulatory Framework Explained

→

Execution Reality

→

Bankability Test

The Strategic Energy Plan is formulated under the 2002 Basic Act on Energy Policy, reviewed roughly every three years, and approved by the Cabinet. It carries no direct legal enforcement — but its targets anchor how regulators, utilities, and investors plan, which is why the numbers matter more than the legal status.

Approved February 2025, the 7th Plan targets carbon neutrality by 2050 and a 73% greenhouse-gas cut by FY2040. Renewables move to around 40–50% of generation, and wind rises from 1.1% (FY2023) to a 4–8% range — the largest proportional jump of any single source.

The plan reaffirms 10 GW of offshore wind by 2030 and 30–45 GW by 2040, supported by promotion zones, the Feed-in Premium (FIP) system, grid prioritization, and domestic supply-chain development. These are the policy levers that turn the headline target into projects.

What the Strategic Energy Plan Is

The Strategic Energy Plan (エネルギー基本計画) is formulated under the Basic Act on Energy Policy, enacted in 2002. It is reviewed approximately every three years and approved by the Cabinet, making it the government’s highest-level roadmap for medium- to long-term energy policy. Every downstream instrument — promotion zone auctions, revenue support schemes, grid planning — is ultimately calibrated against the direction this document sets.

The plan is built around balancing the “S+3E” objectives, the standing evaluation axis for all Japanese energy policy:

- S (Safety) — ensuring public safety as the precondition for everything else

- E (Energy Security) — stable, reliable energy supply

- E (Economic Efficiency) — keeping energy costs and the economy competitive

- E (Environment) — environmental protection and climate action

Reading any individual target — including offshore wind capacity — in isolation misses the point. Each number in the plan is the output of a trade-off across these four axes, which is why the offshore wind figures sit alongside nuclear restarts, thermal phase-down, and hydrogen commercialization rather than standing on their own.

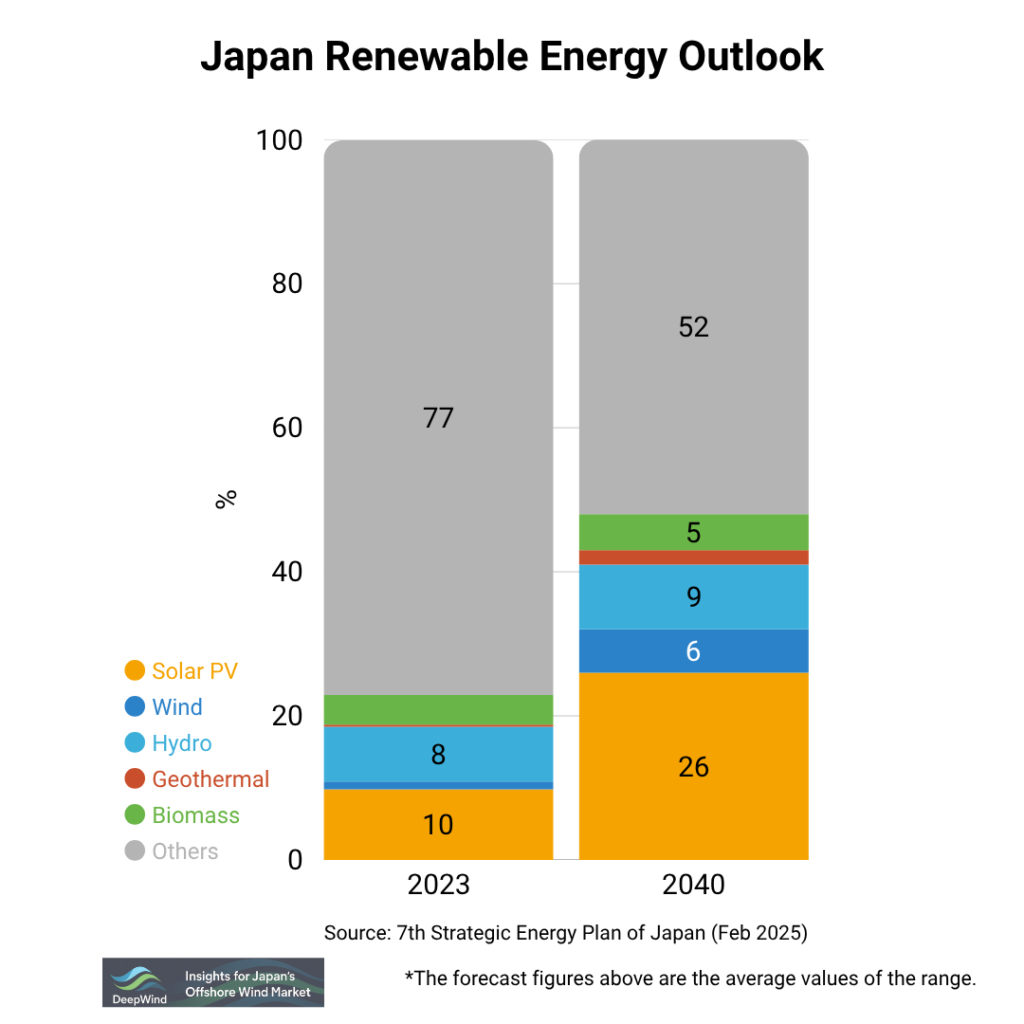

Inside the 7th Plan: the FY2040 Power Mix

The 7th Plan, approved in February 2025, defines a clear path toward carbon neutrality by 2050 and sets a 73% reduction target for greenhouse-gas emissions by FY2040. It maintains the policy of promoting renewables as a primary power source, and quantifies that ambition in a revised FY2040 generation mix.

| Power source | FY2023 (preliminary) | FY2040 (outlook) |

|---|---|---|

| Renewable energy | 22.9% | Around 40–50% |

| Solar | 9.8% | Around 23–29% |

| Wind | 1.1% | Around 4–8% |

| Hydro | 7.6% | Around 8–10% |

| Geothermal | 0.3% | Around 1–2% |

| Biomass | 4.1% | Around 5–6% |

| Nuclear power | 8.5% | Around 20% |

| Thermal power | 68.6% | Around 30–40% |

Two shifts stand out. First, thermal generation roughly halves, from 68.6% to a 30–40% range — the structural space the renewable and nuclear build-out is meant to fill. Second, wind shows the steepest proportional climb of any source: from 1.1% to as much as 8%, a four- to seven-fold increase. Offshore wind is expected to carry most of that growth, because Japan’s onshore wind resource is constrained by terrain and grid access.

Where Offshore Wind Sits in the Plan

Offshore wind is treated as a core pillar of the renewable build-out. The plan reaffirms the government’s standing targets of 10 GW by 2030 and 30–45 GW by 2040 (including floating capacity) — figures first set out in the 2020 Offshore Wind Industry Vision and carried forward here as national policy.

👉 Japan’s Offshore Wind Goals: 10 GW by 2030, 45 GW by 2040

The plan does not just state a target; it points to the policy levers meant to deliver it:

- Promotion Zones and public tenders — the area-designation and auction system that allocates seabed to developers

- Feed-in Premium (FIP) — a market-integrated revenue support mechanism that adds a premium on top of the market price

- Grid prioritization and port infrastructure — connection capacity and base-port development for installation and assembly

- Domestic supply-chain development — support for building a Japanese fabrication and installation industry

Each of these is the subject of its own framework. The revenue model in particular is where many projects live or die, since it determines the price a project can bank on across its operating life.

👉 Japan FIT vs FIP: Renewable Energy Revenue Framework Explained

The longer-term lever is geographic. The 2025 revision of the Renewable Energy Sea Area Act extends the offshore wind permitting system into Japan’s exclusive economic zone (EEZ) — opening the deep-water areas where most of the 2040 capacity, much of it floating, will have to be built.

👉 Japan Expands Offshore Wind Zone to EEZ (2026 Edition)

The Strategic Energy Plan sets direction, not obligation. It does not bind any developer to build, any utility to connect, or any ministry to fund — those commitments live in the downstream auction, FIP, and grid frameworks. The 4–8% wind figure is an outlook, not a guarantee, and the FY2030/FY2040 capacity targets have no penalty attached if missed. Treat the plan as the clearest available statement of government intent, then test each target against execution reality: tender results, grid-connection timelines, and supply-chain readiness.

The plan’s value is as a signal of intent — its credibility is decided downstream.

The Strategic Energy Plan is the cleanest single expression of where Japan says its energy system is going, and the 7th edition’s FY2040 mix gives offshore wind an explicit, quantified place in that future. For anyone allocating capital or planning a supply chain, the document is essential reading precisely because every downstream rule is calibrated against it.

But a target is only as strong as the execution path beneath it. The gap between a 4–8% wind outlook and the projects that would deliver it runs through tender design, grid connection, port capacity, and revenue certainty — none of which the plan itself resolves. The plan tells you the direction of travel; the auction results, FIP terms, and EEZ rollout tell you the speed. Read the plan to understand intent, then watch the implementation frameworks to judge whether the FY2040 numbers are on track or slipping.

Related DeepWind Articles

- Japan’s Offshore Wind Policy & Regulatory Framework Explained

- Japan’s Offshore Wind Goals: 10 GW by 2030, 45 GW by 2040

- Japan FIT vs FIP: Renewable Energy Revenue Framework Explained

- Japan Expands Offshore Wind Zone to EEZ (2026 Edition)

DeepWind Weekly tracks Japan’s offshore wind market beyond headline announcements, focusing on execution risk, cost structure, project viability, supply-chain constraints, and policy implications.

Subscribe to receive weekly intelligence on Japan’s offshore wind market.