Published: January 26, 2026 | Updated: June 22, 2026

POLICY & REGULATION

Japan’s Long-Term Decarbonization Power Supply Auction (LTDA) pays annual capacity revenue (JPY/kW/year) rather than energy revenue (JPY/kWh) — guaranteeing recovery of fixed costs over a 20-year period. Offshore wind is eligible only for Round 2 and Round 3 as a transitional measure. Approximately 90% of market-derived revenue must be returned to the system, limiting upside but eliminating the downside risk that makes project financing difficult under FIP alone.

👉 Japan’s Offshore Wind Policy & Regulatory Framework

→

Execution Reality

→

Bankability Test

FIT and FIP both reward generation volume. LTDA pays a contractually fixed annual capacity revenue for 20 years, creating a cash flow stream independent of output volume. In project finance, this narrows the P50–P90 revenue gap and supports DSCR ≥ 1.35x — a threshold FIP-only projects struggle to meet at current prices.

LTDA eligibility for offshore wind is a time-limited exception for Round 2 and Round 3. Round 4 and beyond are excluded by design. Market revenue from JEPX, ΔkW balancing, non-fossil certificates, and PPA equivalent is approximately 90% returned — LTDA is not a high-yield model; it is a fixed-cost floor.

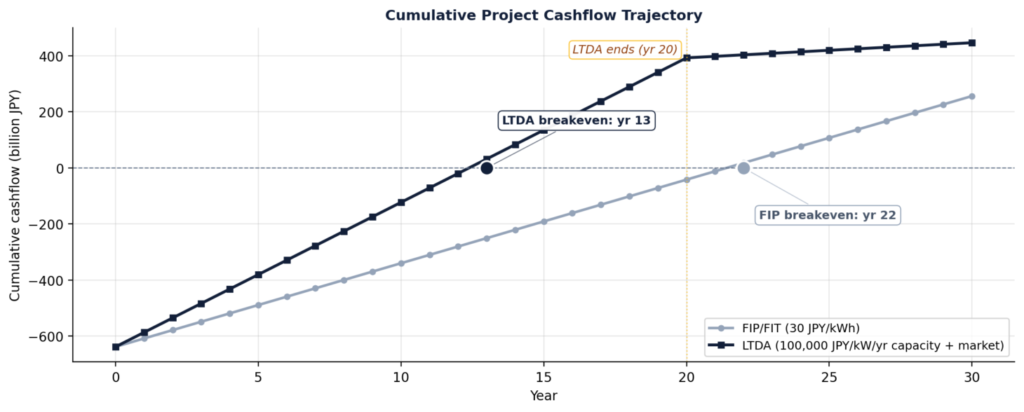

DeepWind’s latest cost model (May 2026) shows the Murakami–Tainai project reaching its break-even point in approximately 13 years at a bid price of JPY 100,000/kW/year. If capacity payments continue for 20 years, the project comfortably exceeds the profitability threshold.

1. The Core Mechanism: Paying for Capacity, Not Output

The Long-Term Decarbonization Power Supply Auction (LTDA) was introduced to solve a structural problem in Japan’s energy transition: decarbonized power sources — offshore wind, nuclear, large-scale hydro — require enormous up-front capital, but Japan’s power market does not provide the long-term revenue visibility that project finance requires.

The core design response is to separate fixed-cost recovery from energy revenue. Under LTDA:

- Winning bidders receive an annual capacity payment (JPY/kW/year) for 20 years

- Payment is based on installed capacity (kW), not generation volume (kWh)

- This payment is designed to cover CAPEX amortization and fixed O&M costs

Government documents describe the scheme as “a mechanism that guarantees a level of capacity revenue equivalent to fixed costs.” The effect is to convert what would otherwise be a merchant revenue stream into a contracted, volume-independent cash flow — dramatically improving bankability for capital-intensive projects.

2. How LTDA Differs from FIT and FIP

FIT and FIP both reward energy output. LTDA rewards capacity availability. That distinction reshapes the entire financial structure of a project.

| Scheme | Revenue Basis | Market Exposure | Primary Objective |

|---|---|---|---|

| FIT | kWh (fixed purchase price) | None | Accelerate early renewable deployment |

| FIP | kWh + market premium | Partial (market-linked) | Integrate renewables into the wholesale market |

| LTDA | kW (capacity value) | Yes — but market upside and downside are largely neutralized | Stabilize long-term investment in decarbonized power |

Under FIT, the generator is fully insulated from wholesale prices. Under FIP, the generator sells into the market and receives a premium above a reference price — carrying price risk but able to capture upside. Under LTDA, the generator participates in the market but returns ~90% of what it earns there; in exchange, it receives a stable capacity payment that covers costs regardless of market conditions.

Japan’s offshore wind auctions shifted from FIT (Round 1) to FIP (Round 2 onward). Round 3 bids came in at effectively zero premium — meaning revenue depends almost entirely on the wholesale price generators can capture. LTDA emerged as the mechanism to restore fixed-cost coverage that zero-premium FIP cannot provide.

👉 Japan’s Offshore Wind Policy Enters a New Phase

3. The 90% Revenue Return Rule — Capping Upside to Guarantee Fixed-Cost Recovery

LTDA’s most distinctive operational feature is the revenue return mechanism. Approximately 90% of all market-derived revenue must be returned to the system.

Revenue streams subject to return include:

- JEPX (Japan Electric Power Exchange) spot market income

- ΔkW balancing market income

- Non-fossil value certificate revenue

- PPA revenue equivalent to market prices

The generator retains approximately 10% of market revenue. In exchange, it receives the full capacity payment designed to cover fixed costs. The trade-off is explicit: accept a ceiling on revenue upside; receive a floor on cost recovery.

LTDA creates a structural tension with corporate PPAs. Any PPA priced above the market reference is treated as “other market revenue” — approximately 90% of the premium above market is returned. High-margin PPAs therefore do not improve the generator’s economics under LTDA. The scheme is designed for cost recovery, not profit optimization.

4. LTDA Eligibility for Offshore Wind: Round 2 and 3 Only

The latest government documents are explicit about offshore wind’s eligibility under LTDA:

- Round 1: Not eligible

- Round 2 and Round 3: Eligible as a temporary exceptional measure

- Round 4 and beyond: LTDA participation is not envisioned

This boundary reflects a deliberate policy design choice. Allowing LTDA access to all future offshore wind rounds would distort bidding strategy by creating a floor that removes the competitive pressure that drives price discovery. Restricting it to Round 2 and 3 acknowledges that those projects — committed before Japan’s cost and rate environment deteriorated — need stabilization support to reach completion.

Round 4 and subsequent auctions will operate under FIP only. Whether developers can submit commercially viable bids under that structure — without an LTDA capacity floor — is the central question for Japan’s next offshore wind policy cycle.

Accessing LTDA capacity revenue requires winning a bid at or below the price cap and meeting capacity factor requirements. Projects that experience significant construction delays or equipment underperformance may risk losing capacity payment eligibility — turning what was intended as a financial floor into a conditional backstop.

5. Price Cap vs. Actual Bid Level

METI documentation sets the following price caps for offshore wind under the third LTDA auction round:

- Price cap: JPY 180,655–200,000/kW/year

This ceiling is a regulatory maximum, not an expected clearing price. DeepWind’s analysis indicates that the actual capacity revenue offshore wind developers need to recover fixed costs is approximately JPY 100,000–120,000/kW/year — roughly 50–60% of the cap.

The wide gap between cap and practical need reflects deliberate buffer against cost uncertainty. In competitive auctions, clearing prices should converge toward the economic break-even level — not the regulatory ceiling.

6. Capacity Factor Requirements Are Being Formalized

The latest government documents explicitly require:

“Generators must achieve annual capacity factors appropriate for each power source.”

For offshore wind, specific thresholds remain under discussion. However, the direction of travel is clear: capacity factor performance will become a formal condition for receiving capacity payments.

For project finance, this introduces a compliance risk layer. Capacity factors for offshore wind depend on site wind resources and turbine availability — both subject to P90 modeling uncertainty. Lenders assessing LTDA-eligible projects will need to stress-test capacity factor scenarios to confirm that the 90th percentile performance band still meets the eligibility threshold.

7. Profitability in Practice: The Murakami–Tainai (690 MW) Case Study

DeepWind uses the Murakami–Tainai offshore wind project (Niigata Prefecture) as a reference case for LTDA profitability analysis. The project — led by Mitsui & Co. and Osaka Gas — is a Round 2 fixed-bottom project that illustrates how LTDA economics work under current market conditions.

Updated Configuration (January 2026 Revision)

In January 2026, the project consortium announced a turbine revision: the original 18 MW GE Vernova turbines (discontinued) would be replaced by 46 units of 15 MW turbines. DeepWind’s cost model (May 2026) reflects this configuration:

- CAPEX: approximately JPY 640 billion (estimated)

- OPEX: approximately JPY 19 billion per year (estimated)

- Capacity: 690 MW

- Operating period: 30 years (assumed)

Scenario: Bid at JPY 100,000/kW/year

- Capacity revenue: approximately JPY 69 billion per year

- Market revenue: ~90% returned → approximately 10% retained (excluded from base calculation)

The case study shows that, at a bid price of JPY 100,000/kW/year, cumulative capacity revenue covers cumulative fixed costs at approximately year 13. If capacity payments continue for 20 years, the project substantially exceeds the breakeven threshold. This confirms that LTDA capacity revenue — not merchant FIP income — is what makes Round 2 project finance viable at current cost levels.

Under LTDA, capacity revenue is treated in project finance as a contractual, volume-independent cash flow. Unlike FIP revenue — which fluctuates with wholesale prices — capacity payments provide a stable base that lenders can model with high confidence. For a 690 MW Round 2 project at JPY 100k/kW/year, the annual capacity revenue of approximately JPY 69 billion provides a floor that absorbs most of the fixed-cost burden, narrowing the P50–P90 revenue spread and supporting DSCR ≥ 1.35x under current lender risk appetite in Japan.

8. What LTDA Means for Developers and Offtakers

Developer Perspective

| Dimension | Benefit | Constraint |

|---|---|---|

| Revenue certainty | Capacity payments guarantee fixed-cost recovery for 20 years | ~90% of market upside is returned to the system |

| Financing | Improved bankability — easier to meet DSCR thresholds | Capacity factor compliance risk if performance falls short |

| PPA strategy | Low default risk makes generator an attractive PPA counterparty | High-margin PPAs do not improve developer economics |

Offtaker Perspective

For offtakers seeking long-term corporate PPAs, LTDA-supported generators offer a specific advantage: the generator’s fixed-cost burden is already covered by capacity revenue, meaning default risk is structurally lower. The PPA is an overlay on an already-stable revenue base — not a lifeline for a financially stressed project.

The constraint for offtakers is that the generator has limited room to offer favorable PPA pricing. With most market-equivalent revenue returned under LTDA, the economics of above-market PPA terms are largely nullified on the generator side.

👉 What Is a Corporate PPA? Japan Market Guide

9. LTDA and Corporate PPAs — A Structural Tension

LTDA and corporate PPAs operate at partial cross-purposes. Under LTDA, any PPA priced above the market reference is treated as “other market revenue” — with approximately 90% returned to the government. The implication: a developer cannot meaningfully improve economics by negotiating a high-margin PPA on top of LTDA capacity revenue.

This does not eliminate the value of PPAs for LTDA-eligible projects. Rather, it changes the nature of the relationship:

- PPAs on LTDA projects are stability arrangements, not yield-enhancement tools

- The offtaker gains a counterparty with very low default risk

- The developer gains a stable demand relationship without dependence on spot market liquidity

The structural tension becomes relevant if an offtaker expects a high-yield, below-market PPA price in exchange for long-term commitment. That incentive structure does not function when 90% of the revenue gap between PPA price and market reference is returned to the system.

Japan’s 2050 grid expansion plans add another layer of context: LTDA-supported large-scale offshore wind is expected to contribute to system stability, and the long-term grid build-out creates a supportive environment for the 20-year project timelines LTDA is designed to cover.

👉 Japan’s 2050 Grid Master Plan Review: Offshore Wind Scenarios

LTDA is a financial architecture tool, not a subsidy — and its termination after Round 3 is the real test for Japan’s offshore wind bankability.

The government’s goal is not to fund offshore wind directly. It is to change the risk profile of the revenue stream well enough that lenders can model it. Capacity revenue that is contractually fixed for 20 years converts what would otherwise be a merchant project into something closer to a contracted project. For Round 2 and 3 projects that bid at near-zero FIP premiums, LTDA capacity revenue may be the difference between a DSCR above 1.35x and one that falls below the bankable threshold.

The harder structural question is Round 4 and beyond. The government has signaled that LTDA will not extend to future offshore wind rounds — meaning new projects must clear an economic hurdle on FIP alone, without a capacity floor. Whether developers can bid commercially viable prices under that structure depends on how much Japan’s offshore wind cost curve moves before the next auction opens. The absence of LTDA is already a central design constraint for the Round 4 policy framework — and the answer to whether it works will define the next decade of Japan’s offshore wind development.