Published: July 9, 2026 | Updated: July 9, 2026

COST & COMMERCIAL VIABILITY

BP is reportedly in talks to leave the 450 MW Yuza offshore wind project in Yamagata — one of two zones Japan awarded in its Round 3 auction in December 2024. The Marubeni-led consortium is reported to continue, and BP says nothing has been decided, so the exit should be read as reported, not confirmed. The more durable story sits underneath the headline. Yuza was won with a zero-premium bid — the same structure every Round 3 winner used — and that structure is what makes these projects difficult to finance, regardless of which partner stays or leaves. The question worth asking is not why BP might exit, but whether a zero-premium award was financeable in the first place, and what could change that.

👉 Offshore Wind Cost Structure and Economics in Japan

→

Execution Reality

→

Bankability Test

In Round 3, all seven bidders bid at the ¥3/kWh floor, so winners were chosen on delivery capability, not price. A zero-premium project earns close to merchant or PPA prices with almost no subsidy top-up, which means the developer absorbs nearly all of the price risk across a roughly 30-year operating life.

Mitsubishi Corporation exited its Round 1 sites in August 2025; BP is now reportedly stepping back from Yuza. The actors are different — a Japanese trading house and a global oil major — but the economics being tested are the same, and elevated CAPEX makes them tighter.

In an illustrative DeepWind Simulator run, the same Yuza site is only borderline bankable under a merchant/FIP path but comfortably bankable under a 20-year LTDA capacity payment. The policy step that would allow that offtake for zero-premium projects is now in public comment.

What Yuza actually is: a 450 MW zero-premium award

The Yuza zone, off the town of Yuza in Yamagata Prefecture, was one of two areas awarded in Japan’s third offshore wind auction (Round 3), announced in December 2024. The winning bidder — a consortium led by Marubeni with Kansai Electric Power, Tokyo Gas, and local partners — plans 30 turbines of 15 MW each (Siemens Gamesa) for a total of 450 MW, targeting commercial operation in June 2030. Our Yamagata Yuza project overview sets out the full scope, timeline, and CAPEX/OPEX assumptions in more detail.

| Project / Area | Yuza Offshore Wind (Yamagata) |

|---|---|

| Capacity | 450 MW (30 × 15 MW) |

| Auction | Round 3, awarded December 2024 |

| Revenue basis | FIP, zero-premium bid (¥3/kWh floor) |

| Target COD | June 2030 |

| Status | BP’s exit reported (Nikkei, July 2026); consortium reported to continue |

| Key commercial issue | Merchant/PPA price risk under a zero-premium structure |

The detail that matters most is the pricing. In Round 3, every one of the seven bids came in at the ¥3/kWh floor — the lowest allowed — so price could not separate the field, and selection came down to non-price criteria such as how credibly each bidder could deliver. Yuza, in other words, was not won on an aggressive number that one company overreached to hit. Zero premium was the entry ticket for everyone.

Why zero premium is a financing problem, not a price win

Under Japan’s Feed-in Premium (FIP) system, a project’s revenue is the market price plus a premium equal to the gap between a fixed base price and a market reference price. A zero-premium bid sets the base price at roughly the reference-price level, which means the premium is close to nothing. In practice the project earns market or corporate-PPA prices with little or no subsidy top-up, and the developer carries almost all of the price risk across the life of the asset. For a deeper walk-through of that revenue mechanism, see our guide to how FIT and FIP actually pay an offshore wind project.

That risk allocation is exactly what lenders scrutinize. Project finance sizes debt against the cash flow a project can be relied on to produce in a downside case — the P90 energy yield, tested through the Debt Service Coverage Ratio (DSCR). When revenue depends on merchant and PPA prices rather than a fixed 20-year offtake, the downside case widens, the DSCR falls, and the financeable amount of debt shrinks. Add steel and equipment costs that remain elevated, and a zero-premium structure leaves very little headroom for CAPEX inflation, currency movement, or schedule slip.

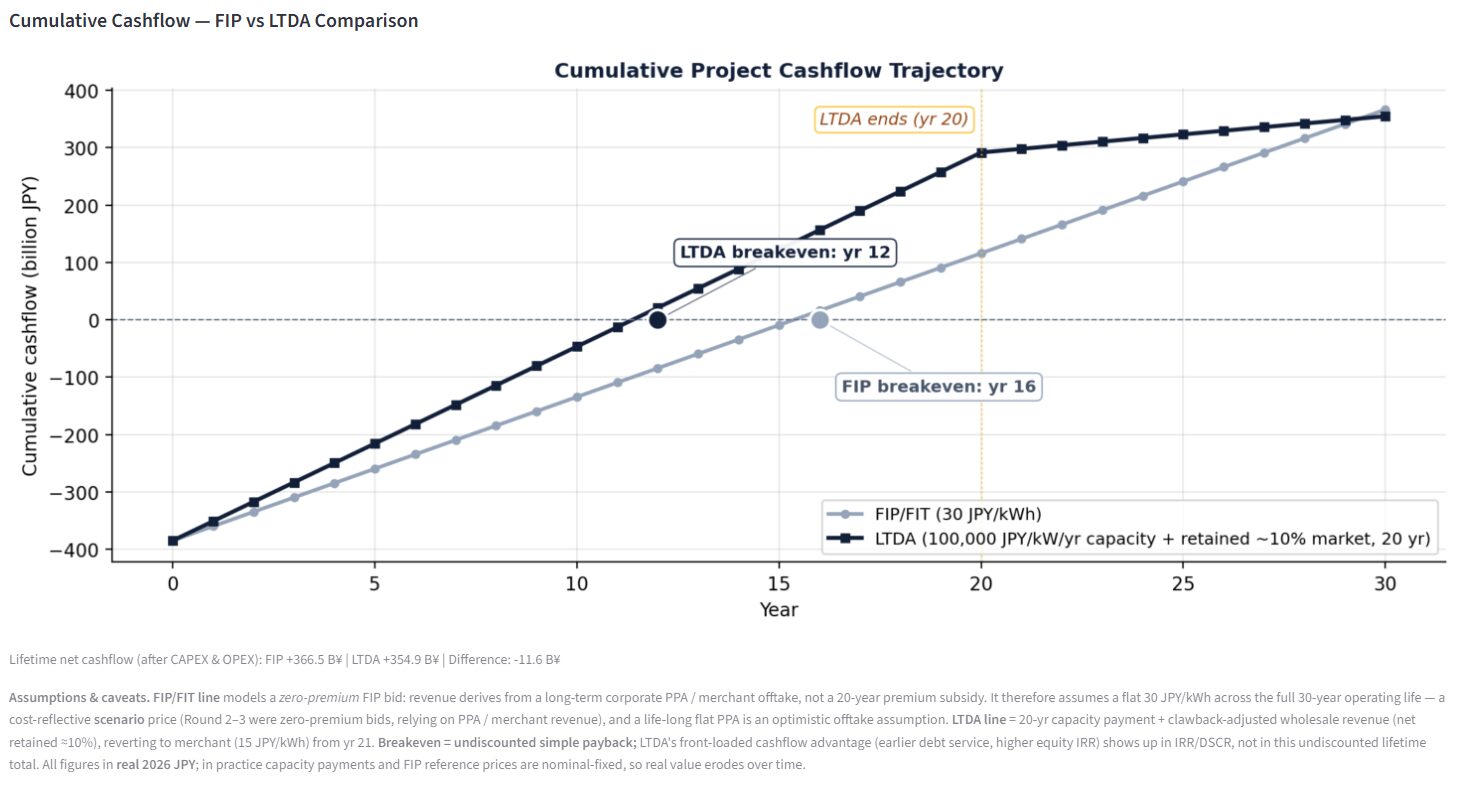

In an illustrative DeepWind Simulator run of the Yuza site (450 MW, real 2026 JPY), a cost-reflective FIP/merchant revenue path produces a minimum DSCR of about 1.33 and a simple payback near year 16 — inside the borderline 1.20–1.35x band, financeable only with negotiation, lower leverage, or additional risk mitigation. These are model outputs on DeepWind assumptions, not the project’s own figures, and are indicative rather than a project-specific forecast. The point is the direction, not the decimal: a zero-premium structure sits close to the edge of the bankable zone before any single risk materializes.

This is why the pattern across Japan matters more than any one company. Mitsubishi Corporation walked away from its three Round 1 sites in August 2025; BP is now reportedly stepping back from Yuza. One is a Japanese trading house, the other a global oil major that has been scaling back offshore wind worldwide — very different motives are possible. But both projects sit on the same side of the same test, and that is the structural signal.

What changes the test: a 20-year LTDA capacity payment

The financeability gap is not fixed. What most directly changes it is the offtake structure — and Japan is now consulting on exactly that. The government has proposed allowing Round 2 and Round 3 zero-premium projects to participate in the Long-Term Decarbonization Auction (LTDA), which pays a fixed capacity revenue in yen per kW per year for 20 years rather than energy revenue per kWh. For a project whose problem is merchant price risk, a long-dated capacity payment is close to the ideal fix: it replaces the volatile part of the revenue with a contracted one, exactly where lenders size the downside.

The same illustrative Simulator run shows the effect. Holding the site, the turbines, and the CAPEX constant and changing only the offtake to a 20-year LTDA-style capacity payment moves the minimum DSCR to roughly 1.80 and pulls simple payback forward to around year 12 — from borderline to comfortably bankable. Nothing physical changed; only the revenue structure did.

Figure 1: Yuza cumulative cashflow — FIP vs LTDA

Same site, same CAPEX; only the offtake structure differs. The LTDA path front-loads cash and reaches breakeven earlier (~year 12 vs ~year 16), lifting the minimum DSCR from ~1.33 to ~1.80.

Source: DeepWind Viability Simulator (illustrative; real 2026 JPY). Not a project-specific forecast.

The LTDA route for zero-premium Round 2 and Round 3 projects is a proposal in public comment, not a settled rule, and the ceiling price for offshore wind in the next auction has not yet been set. Policy can open an offtake option, but it cannot make it usable on its own: if the ceiling is set too low, the route exists on paper but not in practice. Whether this narrows the financeability gap depends less on the headline availability of the LTDA than on the number the government eventually puts on it.

Reading BP’s reported exit

None of this explains BP’s specific decision, and it is not meant to. BP has not stated a reason, the reporting is unconfirmed, and a global major recalibrating its worldwide portfolio can be moving for reasons that have nothing to do with any single site. The useful reading is narrower and more durable: a project structured on zero premium carries a bankability question from the day it is awarded, and that question does not depend on whether BP stays or goes. Consider it a prompt to look at the structure, not a verdict on a company — and certainly not a comment on whether any bid should or should not have been made.

Winning an auction and clearing the bankability test are two different tests — and Japan’s zero-premium rounds settled only the first.

Because every Round 2 and Round 3 bid came in at the floor, these auctions selected for delivery capability, not for financeability. Financeability was assumed to follow. BP’s reported step-back at Yuza is a reminder of how much weight that assumption carries: the same structure that made the auction easy to win makes the project hard to finance.

What matters next is not the BP headline but the policy plumbing behind it. If zero-premium Round 2 and Round 3 projects gain access to a 20-year LTDA capacity payment on workable terms, the financeability gap narrows for precisely the projects most exposed today. If the offshore ceiling price is set too low, the option exists without being used. That decision — not any single investor’s exit — is the variable that will most shape whether Japan’s awarded pipeline actually reaches construction.